The Data Center Bottleneck No One Wants to Price In

How energy availability, interconnection delays, and execution complexity are redefining where hyperscale and AI infrastructure gets built in the United States

Introduction: A Structural Shift in Data Center Development

The data center industry is undergoing a fundamental structural transformation that is no longer driven primarily by real estate fundamentals, but by infrastructure constraints tied directly to energy systems. What once revolved around land acquisition, tax incentives, and geographic positioning has now shifted toward a far more complex equation involving power availability, transmission capacity, and interconnection timelines. This shift is not incremental but systemic, redefining how digital infrastructure is evaluated, financed, and executed. As demand from cloud computing, artificial intelligence workloads, and hyperscale deployments accelerates, the limitations of physical grid infrastructure are becoming increasingly visible.

In this new environment, development timelines are no longer dictated by construction speed alone, but by upstream utility readiness and regulatory alignment. Even well-capitalized projects with secured land can stall for years if grid capacity is constrained or interconnection queues are saturated. This has introduced a new category of risk into the industry: infrastructure latency. Understanding this shift is essential for developers, investors, and operators who are now navigating a market where power is the primary gating factor rather than land or labor.

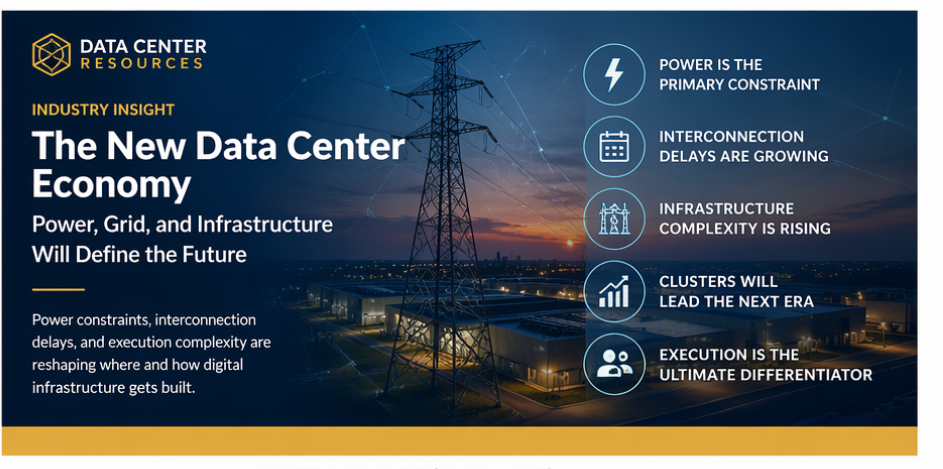

Why Power Availability Is the Primary Constraint in Data Center Growth

Power availability has become the single most important determinant in modern data center site selection and development feasibility. Unlike land, which can be purchased and zoned, electrical capacity is governed by physical grid limitations and long-term utility planning cycles that often extend multiple years into the future. Substations, transmission corridors, and distribution infrastructure all operate within tightly regulated systems that cannot be quickly scaled to meet sudden demand. As a result, even highly attractive geographic locations may be functionally unusable if sufficient megawatt capacity cannot be delivered.

The complexity increases further when considering interconnection agreements, which require extensive engineering studies, load impact assessments, and utility coordination. These processes are not standardized across regions, meaning timelines and requirements vary significantly depending on jurisdiction. In many cases, the interconnection queue itself becomes the largest source of delay in the entire development lifecycle. This creates a structural mismatch between the speed of digital demand growth and the slow-moving nature of physical grid expansion.

The Grid Interconnection Bottleneck and Utility Constraints

Behind every data center project lies a complex interconnection process that determines how energy is delivered from the grid to the facility. This process involves coordination between developers, utilities, regional transmission organizations, and regulatory bodies, all of which must align before power can be formally allocated. In many regions across the United States, interconnection queues are already backlogged due to rapid increases in energy demand from industrial electrification, renewable integration, and hyperscale computing growth.

The challenge is compounded by the fact that grid infrastructure was not originally designed for the current level of concentrated digital load. Substations that once supported regional commercial use are now being asked to support multi-hundred-megawatt or gigawatt-scale campuses. This mismatch between legacy infrastructure design and modern demand requirements creates a structural bottleneck that cannot be resolved through capital alone. Instead, it requires coordinated long-term planning between public utilities and private developers.

Substations, Transmission Lines, and the Physical Reality of Power Delivery

At the core of every data center’s feasibility lies the physical reality of how power is transmitted and transformed. Substations act as the critical interface between high-voltage transmission lines and usable distribution power for large-scale infrastructure. However, substation capacity is not infinitely scalable and often requires significant engineering, land acquisition, and regulatory approval to expand. In many cases, the timeline for substation development becomes a defining factor in whether a project is viable within a reasonable horizon.

Transmission infrastructure presents an additional layer of constraint, as high-voltage lines must be routed across long distances to connect generation sources to demand centers. These corridors are often subject to environmental review, land rights negotiations, and multi-agency approval processes. The result is a deeply interconnected system where even minor constraints in one segment can ripple across the entire development timeline. This reinforces the importance of early-stage power intelligence in evaluating site viability.

Permitting, Regulation, and Jurisdictional Friction

Beyond physical infrastructure, regulatory and permitting frameworks introduce another layer of complexity into data center development. Local, state, and federal jurisdictions each maintain distinct approval processes, which can significantly influence project timelines. In some regions, permitting may be streamlined to encourage infrastructure investment, while in others it may involve extended environmental review, zoning challenges, or public consultation requirements. This variability creates a fragmented development landscape where execution speed is heavily dependent on geography.

The permitting process becomes even more complex in adaptive reuse scenarios, where existing industrial or commercial facilities are converted into data center infrastructure. These projects often require reclassification of land use, upgrades to electrical systems, and compliance with updated safety and environmental standards. While adaptive reuse can accelerate development compared to greenfield builds, it still requires careful navigation of regulatory frameworks. Understanding these dynamics is critical for aligning development timelines with market demand.

Execution Complexity: Where Data Center Projects Are Won or Lost

Even when land, power, and permits are secured, execution remains one of the most challenging phases of data center development. The construction process involves tightly coordinated systems including civil engineering, electrical infrastructure, cooling systems, backup generation, and high-voltage integration. Each of these components must be sequenced correctly to avoid cascading delays or cost overruns. Small inefficiencies in coordination can quickly escalate into significant project disruptions.

Execution complexity increases further in hyperscale environments, where multiple contractors and engineering teams must operate in parallel under compressed timelines. The integration of substations, switchgear, and high-density compute environments requires precise technical alignment across disciplines. As infrastructure density increases, the margin for error decreases significantly. This makes execution capability not just an operational function, but a strategic differentiator in the industry.

The Rise of Data Center Clusters and Super-Regional Infrastructure Zones

A major structural shift emerging in the industry is the development of data center clusters, where multiple facilities are co-located within high-capacity power regions. These clusters, sometimes referred to as super-regional infrastructure zones, allow developers to leverage shared transmission infrastructure and optimize grid investment across multiple assets. This approach increases efficiency while enabling scalability for long-term hyperscale demand growth.

However, clustering also introduces new coordination challenges between developers, utilities, and infrastructure planners. Managing shared grid capacity requires careful allocation strategies and long-term forecasting of energy demand. In regions where clustering is successful, entire ecosystems of digital infrastructure are forming, attracting both capital investment and cloud providers. This trend is reshaping the geographic distribution of digital infrastructure across the United States.

Artificial Intelligence and the Acceleration of Energy Demand

The rapid expansion of artificial intelligence workloads is placing unprecedented pressure on existing data center infrastructure. AI training and inference workloads require significantly higher energy density compared to traditional cloud computing applications. This shift is accelerating demand for large-scale facilities capable of supporting continuous high-performance compute operations. As a result, power demand forecasts are being revised upward across nearly all major hyperscale markets.

This acceleration is exposing the limitations of existing grid infrastructure at a faster pace than anticipated. Utilities are now facing compounding demand from multiple sectors simultaneously, including transportation electrification, industrial growth, and digital infrastructure expansion. The convergence of these demand streams is creating a new energy constraint environment that will define the next decade of infrastructure development.

Strategic Implications for Developers and Investors

For developers and investors, the implications of these shifts are significant. Site selection can no longer rely on traditional real estate metrics alone and must incorporate deep analysis of power availability, interconnection timelines, and infrastructure scalability. Projects that fail to account for these variables risk extended delays or structural infeasibility. This has elevated the importance of integrated infrastructure strategy as a core competency in the industry.

At the same time, capital allocation strategies are evolving to reflect longer development timelines and higher infrastructure complexity. Investors are increasingly prioritizing partners who can demonstrate execution capability across the full development lifecycle, from site identification to energized delivery. This shift is redefining how risk is evaluated and how infrastructure assets are underwritten in the modern market.

Conclusion: Infrastructure Is Now the Defining Constraint of Digital Growth

The evolution of data center development reflects a broader transformation in how digital infrastructure is built, financed, and constrained. Power availability, grid capacity, and execution capability have emerged as the dominant variables shaping industry growth. In this environment, traditional real estate frameworks are no longer sufficient to evaluate project viability. Instead, a systems-level understanding of infrastructure is required.

As demand continues to accelerate, the gap between digital growth and physical infrastructure capacity will become increasingly pronounced. The companies that succeed in this environment will be those that understand not just where to build, but how infrastructure systems actually function at scale. Ultimately, execution—not intention will determine outcomes in the next era of data center development.