The Grid Is the New Waterfront: Why Transmission Access Is Quietly Repricing American Land

There is land.

There is power.

And increasingly, there is a widening gap between the two.

For decades, land valuation in the United States followed familiar logic: proximity to population centers, highway access, water rights, zoning flexibility, development trajectory. The formula was stable enough to teach in business schools and predictable enough to model in spreadsheets.

That model is becoming incomplete.

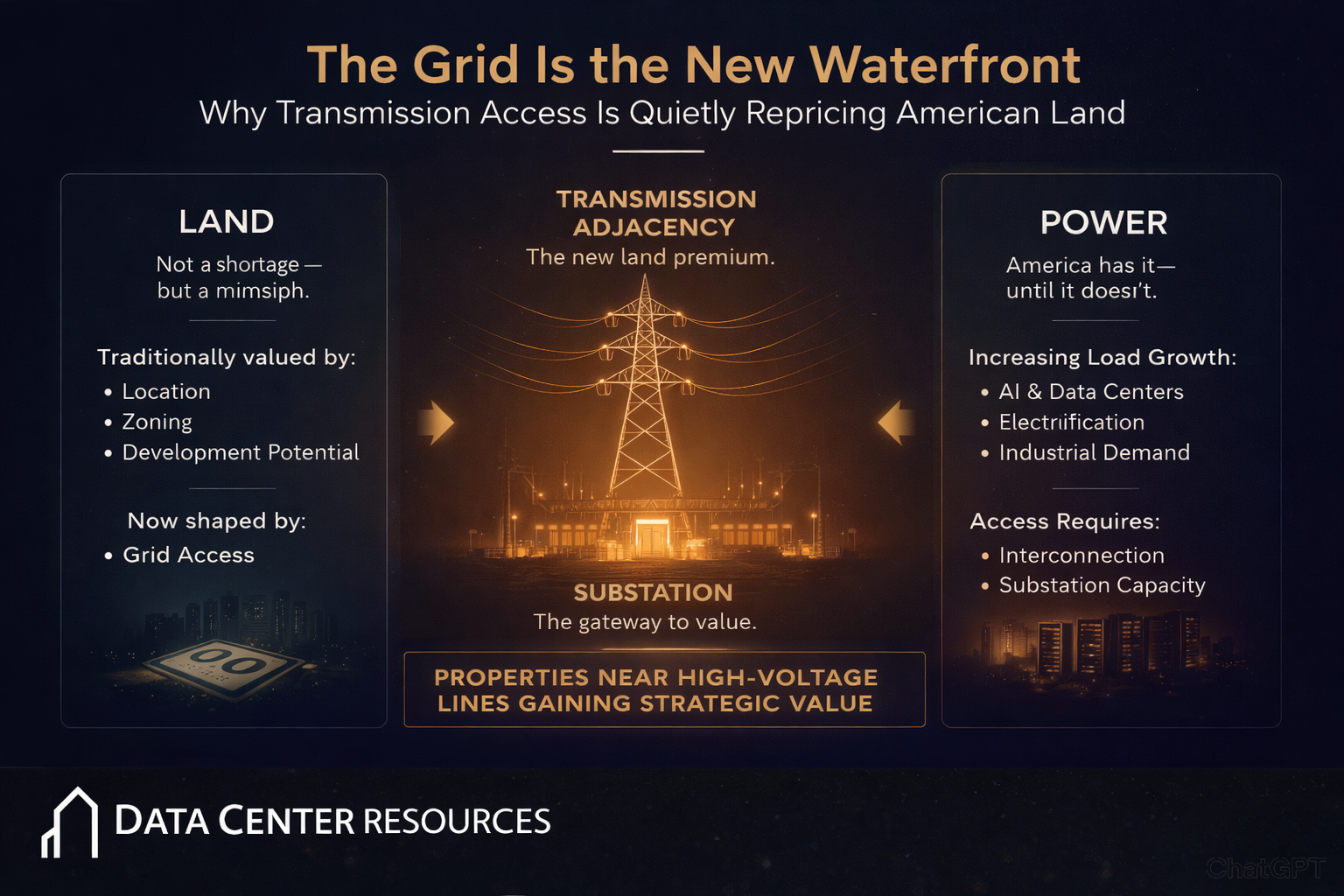

In 2026, a more subtle force is shaping land economics: grid access.

Not merely electricity availability — but transmission adjacency, substation capacity, interconnection feasibility, and the regulatory pathways that determine whether electrons can move from generation to load.

The land hasn’t changed.

The grid has.

And the grid is tightening.

A New Constraint Emerges

America is not running out of acreage. It is running into power bottlenecks.

Artificial intelligence training clusters, hyperscale data centers, advanced manufacturing reshoring, electrified transportation, and distributed generation have all converged on the same physical limitation: transmission infrastructure.

The Federal Energy Regulatory Commission (FERC) has documented swelling interconnection queues across major markets. Regional Transmission Organizations (RTOs) are processing record volumes of generation requests. Utilities are revising load forecasts upward — in some cases dramatically — as AI-related demand shifts from theoretical to real.

In certain regions, projects are facing multi-year delays not because land cannot be acquired, but because grid capacity cannot be secured.

This is not a land shortage.

It is a transmission scarcity.

And scarcity reprices assets.

Land vs. Power: The Decoupling

Historically, land and power were assumed to move together. Industrial parks received substations. Residential subdivisions received distribution feeders. Growth was linear and incremental.

What is unfolding now is nonlinear.

Hyperscale data centers can require 200 to 500 megawatts — sometimes more. That is not incremental demand. That is a medium-sized city arriving in one permitting cycle.

AI workloads, particularly large language model training and inference clusters, intensify this effect. Compute density translates directly into electrical load. Cooling infrastructure compounds it.

Utilities, meanwhile, operate under regulatory frameworks that prioritize reliability and ratepayer stability. Transmission expansion is capital-intensive and politically complex. Rights-of-way are contested. Permitting timelines stretch.

The result is a decoupling:

Land may be abundant.

Power access may not be.

The Interconnection Queue Problem

The interconnection queue — once a niche technical process — has become a market indicator.

In several U.S. regions, generation projects have waited years for approval. Studies reveal that a large percentage of proposed projects withdraw before completion, often due to escalating upgrade costs or uncertainty around timelines.

This phenomenon reveals two realities:

Grid capacity is finite.

The cost of accessing it is rising.

For landowners, this means that mere proximity to transmission lines is insufficient. What matters is viable interconnection.

For developers, it means site control without grid certainty carries structural risk.

For utilities, it means balancing unprecedented load growth against infrastructure limitations and regulatory oversight.

Substations: The Quiet Gatekeepers

The substation is rarely glamorous. It does not carry the political symbolism of a wind farm or the architectural intrigue of a data center campus. It is utilitarian: transformers, switchgear, protective relays, steel lattice, gravel yards.

But economically, it is pivotal.

A substation performs three essential functions:

• Voltage transformation

• Grid interconnection

• System protection and control

Without it, high-voltage transmission cannot be safely integrated into lower-voltage distribution or end-use systems.

More importantly, without substation capacity, generation cannot enter the grid and load cannot be served at scale.

The substation is not just equipment.

It is permission.

It is access.

It is optionality.

AI and the Acceleration of Load Growth

The generative AI boom has introduced a structural shift in load forecasting.

Traditional load growth assumptions hovered around modest annual increases — often 1–2% in mature markets.

AI changes that.

Training clusters can consume hundreds of megawatts continuously. Inference at scale introduces steady baseline demand rather than episodic peaks. Data centers that once required 30–50 MW now contemplate 300+ MW campuses.

Utilities are revising their integrated resource plans accordingly.

In some regions, projected load growth has doubled within a single planning cycle.

This is not merely incremental electrification.

It is industrial-scale digitalization.

And it is powered by transmission.

The Geography of Constraint

Not all regions are equally constrained.

Some markets possess excess transmission capacity due to industrial decline or historical overbuilding. Others are saturated, particularly where renewable generation interconnection has surged.

Sun Belt states, attractive for land availability and tax incentives, may face localized transmission bottlenecks. Northeastern markets contend with permitting complexities. Western grids grapple with wildfire risk and reliability mandates.

The economic geography of the grid is uneven.

Land valuation must increasingly account for that unevenness.

A parcel 200 feet from a high-voltage line may carry more long-term strategic value than a larger tract farther from interconnection points.

The Repricing of “Idle” Land

Idle land has traditionally been viewed as an opportunity cost potential development waiting for capital or zoning changes.

In an energy-constrained environment, idle land near transmission becomes something else:

Strategic reserve capacity.

Even without immediate development, such land carries embedded optionality. It can host:

• Substation expansions

• Generation interconnections

• Battery storage facilities

• Industrial load centers

The value lies not in current use, but in future grid participation.

This reframes land monetization.

Instead of liquidation, owners may consider structured infrastructure agreements that preserve ownership while enabling grid-aligned development.

Utilities Under Pressure

Utilities operate within a regulatory compact: ensure reliability, maintain affordability, and earn a regulated return on invested capital.

Rapid load growth disrupts planning assumptions.

Transmission expansion is capital-heavy. Rate cases are politically sensitive. Infrastructure timelines lag demand surges.

Private substation partnerships and strategically located interconnections can help alleviate localized constraints without requiring system-wide transmission overhauls.

From a utility perspective, the objective is stability.

From a developer perspective, the objective is certainty.

From a landowner perspective, the objective is participation.

These objectives intersect at the substation.

Merchant vs. Regulated Power Dynamics

Energy markets in the United States operate under varied structures:

• Fully regulated utility territories

• RTO-managed wholesale markets

• Hybrid arrangements

In merchant environments, generation sells into competitive markets. In regulated environments, cost recovery follows approved tariffs.

Substation-led development must navigate these frameworks carefully.

Revenue models differ.

Risk allocation differs.

Interconnection timelines differ.

The sophistication required is not trivial.

Grid access is technical.

Grid participation is contractual.

Capital Markets and Infrastructure Appetite

Institutional capital has shown sustained appetite for infrastructure assets over the past decade. Pension funds, sovereign wealth funds, and private equity firms seek long-duration, stable cash flows.

Transmission and substation assets, when structured appropriately, align with these preferences.

They are tangible.

They are regulated or quasi-regulated.

They are essential.

As AI-driven load growth becomes more visible, infrastructure investors may increasingly evaluate grid-adjacent assets as strategic holdings rather than peripheral utilities.

Land near transmission may thus represent embedded infrastructure optionality attractive to capital markets.

Risk, Reality, and Restraint

It is tempting to romanticize grid adjacency as guaranteed value.

That would be inaccurate.

Risks remain:

• Regulatory uncertainty

• Interconnection study costs

• Upgrade requirements

• Community opposition

• Environmental review

Not all land near transmission will become an energy asset.

Not all substations will yield favorable economics.

The repricing is probabilistic, not absolute.

Yet probabilities matter.

Markets price optionality.

And transmission proximity increases optionality.

The Future: Power as the Defining Metric

In prior cycles, proximity to highways defined industrial land value. In coastal cities, waterfront access defined premium pricing.

In the coming decade, high-voltage transmission access may play a similar role in select markets.

Power is becoming the defining input for digital infrastructure, advanced manufacturing, electrified transport, and energy storage.

Without it, projects stall.

With it, capital mobilizes.

The grid is not visible in most real estate marketing materials.

That may change.

Final Observation

There is land.

There is power.

There is an increasingly consequential distinction between the two.

As AI accelerates, electrification deepens, and utilities navigate unprecedented load growth, transmission access becomes less technical detail and more economic determinant.

The substation — once peripheral to property valuation — becomes central.

In quiet, steel-framed yards beneath high-voltage lines, a repricing of American land may already be underway.

Not dramatic.

Not speculative.

But structural.

And structural shifts, once recognized, tend to persist.